- Dec. 01

- Richard Parker

To make your portfolio grow and blossom, just add water

As any gardener knows, the secrets of great returns are patience, diversification . . . and regular weeding

Making your money grow isn’t rocket science — it’s more like gardening, really. For those of us who will never understand advanced physics, it is reassuring that many experts argue all you need for capital growth is patience and some common sense that will be familiar to anyone who has ever tended a flowerbed.

For example, “little and often” is a good rule for watering your plants but it applies just as well to accumulating wealth. Don’t sit in the shade and hope for the best; make regular reviews to nurture success and weed out failures.

Diversification — selecting a range of different species or stocks — will smooth returns and limit your exposure to any single setback. Different flowers or funds will bloom in different seasons or at different stages in the economic cycle.

If all this sounds like a statement of the bleedin’ obvious, consider how many intelligent and successful people make the elementary mistake of investing too much in too few funds or shares. You don’t need to take my word for it — the interviewees say so themselves in Money’s Fame and Fortune feature many times every year.

Those revelations usually come in the part of Fame and Fortune where they are asked whether they prefer pensions or property. Back comes the answer that they will never trust the stock market again, after plunging into half a dozen spiv stocks on the recommendation of a friend before — surprise, surprise — it all went wrong.

Even a senior colleague tells a similar story, but I will spare his blushes here. The important point to remember is that diversification is the simplest and surest way to diminish the dangers inherent in the stock markets — or, indeed, in investing in anything.

Pooled funds — whether they are called investment trusts, unit trusts or exchange-traded funds — offer automatic diversification, because they spread individual investors’ money over dozens of different companies, or different countries in the case of international funds. That way, setbacks or failure in any of the individual underlying assets will not have catastrophic consequences for the fund as a whole or the investor.

Many pooled funds also offer the chance to make regular savings, which diminishes the risk of bad timing, and of investing a lump sum just before share prices fall. They do this by drip-feeding modest sums into the market, month by month. That’s certainly how I got started more than a quarter of a century ago — and the “little and often” approach eventually led to substantial returns.

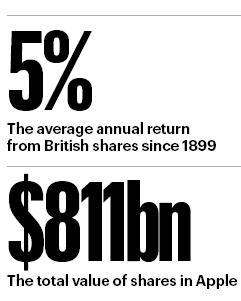

However, it’s only fair to say that, at first, progress seemed painfully slow. For example, 5% growth — the average annual real return from shares — does not add up to much on a small sum of money. However, the same rate of growth on your life savings should be more than enough to fund a year’s expenditure in retirement.

In much the same way, most fruit trees yield a modest harvest — if any at all — in their early years. But after five to 10 years, the crop might well be more than you can eat.

Similarly, taking a medium to long-term approach to achieving your goals is the best way to avoid disappointment. Sreekala Kochugovindan is co-author of the Barclays Capital Equity Gilt Study, perhaps the most comprehensive analysis of returns from various assets. She tells me that shares on the London stock market beat cash deposits three-quarters of the time — provided you remain invested for five years.

The probability of shares beating cash falls to nearer two-thirds — or 68% — if you invest for only two years.

That is why patience is as important for investors as it is for gardeners. Never mind what the speculators or spivs say; it is silly to expect substantial returns from a few days’ trading, just as it is foolish to plant a seed and expect flowers the next day. The poet and novelist Rudyard Kipling, who began work as a journalist before going on to greater things, observed: “Our England is a garden and such gardens are not made by singing ‘Oh, how beautiful’ and sitting in the shade.” Successful gardeners and investors understand that the more you put in, the more you are likely to take out.

Of course, that is all too much bother for those who are happy to pay someone else to do the gardening and investing for them. That’s fair enough, I suppose, although — as someone who enjoys both pursuits — it seems to me a bit like paying someone else to eat your dinner for you.

The similarities even include our age or life stage. Let’s face it, we had more exciting things to do when we were teenagers but, by the time you are old enough to take a close interest in investment, you probably also own a garden.

That’s why M&G, the company that introduced unit trusts to Britain, is the sponsor of the Chelsea flower show, which starts on Tuesday. Sad to say, this will be the last time M&G will fill that role, because such extravagant expenditure is apparently deemed inappropriate in the age of austerity.

Let’s hope leaner marketing budgets don’t mean fewer people benefit from the valuable lessons that something as simple as gardening can teach us about investment.

My own favourite tip is not to waste time worrying about the past, because investment is like growing asparagus: you should always have started five years ago.

For those who failed to do so but would like to enjoy capital growth in future, there is no better time to start than today. Money and gardening go together like strawberries and cream. Make the most of both this summer.

How do you like them apples? The downside of pessimism

Everyone knows who John Wayne was but how many remember Ron Wayne? I only ask because the lesser-known Wayne might prove a better guide for investors today than the drawling gunslinger did.

Ron was a shareholder in a technology start-up just over 40 years ago, along with two friends. Among other things, Ron even drew up the logo for their firm — an elaborate etching of the inventor Isaac Newton, sitting under a tree with an apple overhead.

Then, in 1976, Ron decided he had had enough and sold his stake for $800 to the other founders, Steve Jobs and Steve Wozniak. Today, that techie tiddler has a stock market capitalisation of $800bn (£614bn) and Apple is the most valuable company in the world.

The thing that brings this tale to mind is the reaction of one or two folk to my recent piece about technology shares. I recalled how I tipped Apple here in January last year and picked up shares at $95 that traded at $153 this week. I also mentioned the electric car maker Tesla, tipped here in May last year when I bought shares at $220 that now change hands for $311.

This prompted some teeth-sucking, chin-stroking and wise warnings that it will all end in tears. I am not so sure, although it’s only fair to add that I also reported a bigger holding in Polar Capital Technology investment trust, which provides less risky exposure to this sector than just two companies’ shares. This fund has more than doubled my money over four years.

Here and now, the cautionary tale of Ron Wayne should remind us to beware premature pessimism. Put another way, I would rather have sweet returns from Apple than the cold comfort of sour grapes.